Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When you sell your home on your own, you need to handle Pricing, Marketing, Financing, Negotiating and the Closing. Listen to this week’s edition to discover what to expect.

Real Estate Reflections •

October 31, 2022

Millennials Are Still a Driving Force of Today’s Buyer Demand

If you’re thinking about selling your house but wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for.

While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. Here’s why.

Millennial Homebuying Power

While there’s no denying higher mortgage rates are making it more challenging to afford a home today, many millennials are still eager and able to buy homes – whether it’s their first or they’re moving up. That’s in large part because of the value they place on education.

A recent article from First American says millennials may be the most educated generation in our nation’s history. Because of that, they tend to earn higher wages, and that translates to greater homebuying power. Odeta Kushi, Deputy Chief Economist at First American, explains:

“In 2020, millennials with a bachelor’s degree had a median household income of over $100,000, while those with at least a graduate degree had a median household income of over $120,000. Compare those income levels with the median household income of millennials with just a high school degree (or some college) of $60,000 and the earning power benefits of higher education are undeniable. . . . Millennials’ pursuit of higher education is good news for the housing market. . . because education is the key to unlock both greater earning power and, in turn, homeownership.”

And since wages are one of the key things that factor into affordability when it comes to buying a home, these higher earnings can help millennials achieve their homeownership goals.

Millennials Continue To Be a Driving Force of Demand

A number of studies have looked into how the millennial generation views homeownership and how they’re uniquely positioned to define the housing market moving forward. As the largest generation, the volume of potential millennial homebuyers will have an impact on the market for years to come. As an article in Forbes explains:

“At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.”

If you’re thinking of selling your house but are hesitant because you’re worried that buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As Mark Fleming, Chief Economist at First American, says in an article:

“While not the frenzy of 2021, the largest living generation, the Millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market.”

Bottom Line

Millennials are interested in and well-positioned to achieve their homeownership dreams. If you’re ready to sell your house, know that it may be just what they’re looking for.

Real Estate Reflections • Tips •

October 28, 2022

5 Ways To Sell Your House Quick

Contact me for more details and to book a 15 min consultation, visit RLWRealEstate.com or call me at 817-791-0631.

Real Estate Reflections •

October 11, 2022

The Long-Term Benefit of Homeownership

Today’s cooling housing market, the rise in mortgage rates, and mounting economic concerns have some people questioning: should I still buy a home this year? While it’s true this year has unique challenges for homebuyers, it’s important to factor the long-term benefits of homeownership into your decision.

Consider this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how you gain equity and wealth as home values grow with time.

The National Association of Realtors (NAR) explains:

“Home equity gains are built up through price appreciation and by paying off the mortgage through principal payments.”

Here’s a look at how just the home price appreciation piece can really add up over the years.

Home Price Growth Over Time

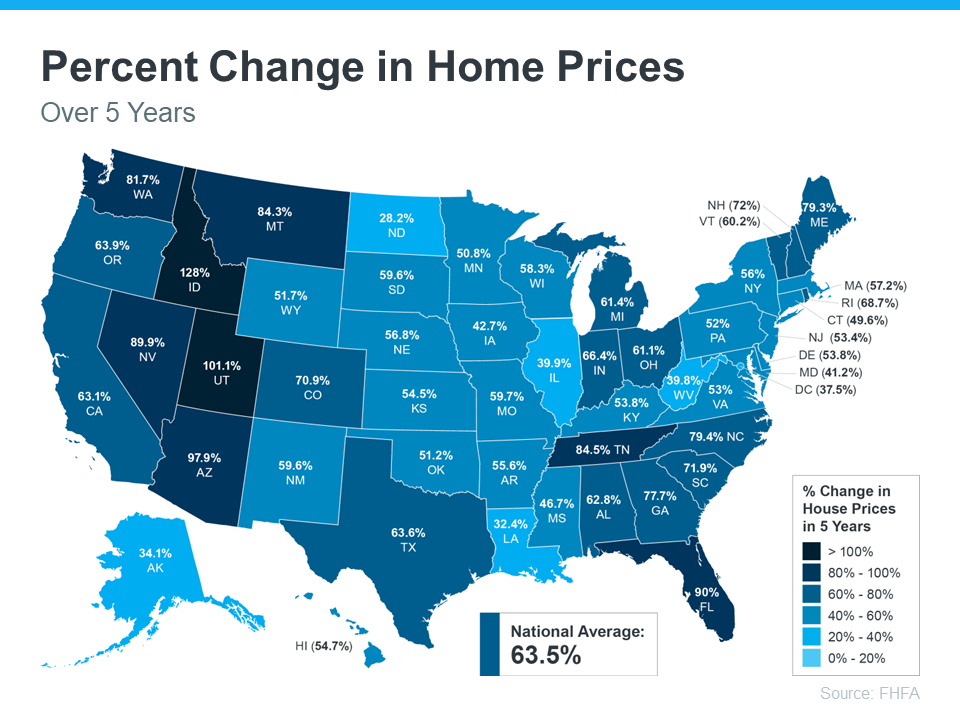

Even though home price appreciation has moderated this year, home values have still increased significantly in recent years. The map below uses data from the Federal Housing Finance Agency (FHFA) to show just how noteworthy those gains have been over the last five years.

If you look at the percent change in home prices, you can see home prices grew on average by almost 64% nationwide over that period.

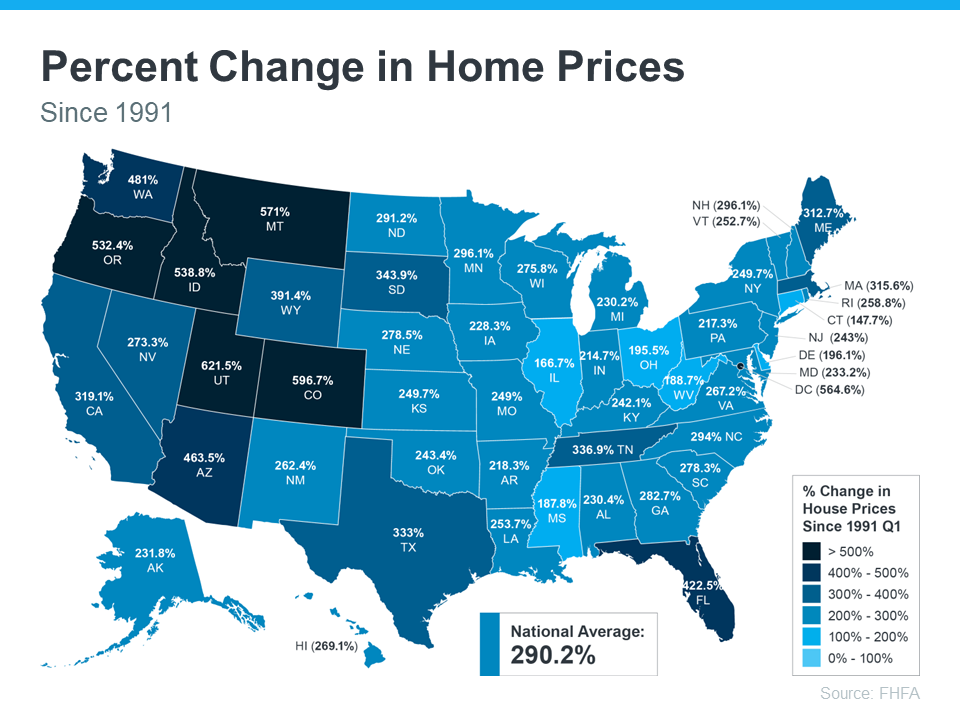

That means a home’s value can increase substantially in a short time. And if you expand that time frame even more, the benefit of homeownership and the drastic gains you stand to make become even clearer (see map below):

The second map shows, nationwide, home prices appreciated by an average of over 290% over roughly a thirty-year span.

While home price growth varies by state and local area, the nationwide average tells you the typical homeowner who bought a house thirty years ago saw their home almost triple in value over that time. This is why homeowners who bought their homes years ago are still happy with their decision.

Even if home price appreciation eases as the market cools this year, experts say home prices are still expected to appreciate nationally in 2023. That means, in most markets, your home should grow in value over the next year even if the pace is slower than it was during the peak market frenzy when prices skyrocketed.

The alternative to buying a home is renting, and rental prices have been climbing for decades. So why rent and fight annual lease hikes for no long-term financial benefit? Instead, consider buying a home. It’s an investment in your future that could set you up for long-term gains.

Bottom Line

Don’t let the shifting market delay your dreams. Data shows home values typically appreciate over time, and that gives your net worth a nice boost. If you’re ready to start your journey to homeownership, let’s connect today.

Real Estate Reflections •

October 9, 2022

Two Questions Every Homebuyer Should Ask Themselves Right Now

Rising interest rates have begun to slow an overheated housing market as monthly mortgage payments have risen dramatically since the beginning of the year. This is leaving some people who want to purchase a home priced out of the market and others wondering if now is the time to buy one. But this rise in borrowing cost shows no signs of letting up soon.

Economic uncertainty and the volatility of the financial markets are causing mortgage rates to rise. George Ratiu, Senior Economist and Manager of Economic Research at realtor.com, says this:

“While even two months ago rates above 7% may have seemed unthinkable, at the current pace, we can expect rates to surpass that level in the next three months.”

So, is now the right time to buy a home? Anyone thinking about buying a home today should ask themselves two questions:

1. Where Do I Think Home Prices Are Heading?

There are two places to turn to answer this question. First is the consensus of what experts are saying. If you look at what experts are projecting for home prices in 2023, they’re forecasting home price appreciation around 2%. While it’s true some are calling for depreciation, most are calling for appreciation in home values over the next year.

The second spot to turn to for information is the Home Price Expectation Survey from Pulsenomics – a survey of a national panel of over one hundred economists, real estate experts, and investment and market strategists. According to the latest release, the experts surveyed are also calling for home price appreciation for the next several years (see graph below):

2. Where Do I Think Interest Rates Are Heading?

Like mentioned above, Ratiu sees mortgage rates rising over the next several months. Another expert agrees. Mark Fleming, Chief Economist at First American, says:

“While mortgage rates are expected to continue to drift higher over the coming months, much of the rapid increase in rates is likely behind us.”

The instability in the world and higher inflation are driving this volatile market, resulting in higher borrowing rates for those looking to buy homes.

Bottom Line

If you’re thinking about buying a home, asking yourself about home prices and mortgage rates will help you make a powerful and confident decision. Experts see both prices and rates rising in the future. The alternative is to rent, but rents are also increasing. That may mean buying a home makes more sense than renting.

Real Estate Reflections • Tips •

September 24, 2022

The 10 Mistakes Buyers Make When Purchasing a Home

Purchasing a home is one of the biggest financial decisions you will make. It is very important to be informed before and stay informed during the process—and make sure you have a good REALTOR® at your side every step of the way.

Here is a list of the 10 most commonly made mistakes buyers make when purchasing a home (as documented by Brian Buffini)

1. Making an offer on a home without being prequalified. Pre-qualification will make your life easier—so take the time to speak with a lender. The lender’s specific questions in regard to income, debt, etc., will help you determine the price range you can afford.

2. Not having a home inspection. Trying to save money today can end up costing you tomorrow. A qualified home inspector will detect issues that many buyers might overlook.

3. Limiting your search to open houses, ads or the Internet. Many homes listed in magazines or on the Internet have already been sold. Your best course of action is to contact a REALTOR®. They have up-to-date information that is unavailable to the general public and are the best resource to help you find the home you want.

4. Choosing a REALTOR® who is not committed to forming a strong business relationship with you. Making a connection with the right REALTOR® is crucial. Choose a professional who is dedicated to serving your needs—before, during and after the sale.

5. Thinking there is only one perfect house out there. Buying a home is a process of elimination, not selection. New properties arrive on the market daily, so be open to all possibilities. Ask your REALTOR® for a comparative market analysis, which compares similar homes that have recently sold, or are still for sale.

6. Not considering long-term needs. It is important to think ahead. Will the home suit your needs 3-5 years from now?

7. Not examining insurance issues. Purchase adequate insurance. Advice from an insurance agent can provide you with answers to any concerns you may have.

8. Not buying a home protection plan. This is essentially a mini insurance policy that usually covers basic repairs you may encounter and can be purchased for a nominal fee. As an item of value, I provide my clients a Home Warranty from Super Home Warranty company ($459 value)

9. Not knowing total costs involved. Early in the buying process, ask your REALTOR® or lender for an estimate of closing costs. Title company and attorney fees should be considered. Pre-pay responsibilities such as Homeowner Association fees and insurance must also be taken into account. Remember to examine your settlement statement prior to closing.

10. Not following through on due diligence. Buyers should make a list of any concerns they have relating to issues such as crime rates, schools, power lines, neighbors, environmental conditions, etc. Ask the important questions before you make an offer on a home. Be diligent so that you can have confidence in your purchase.

Bonus Tip: Being Unrepresented With New Construction. New build salespeople are protecting the interest of their builder, your REALTOR® is protecting your interest, with negotiations, recommended inspections, etc.

If you are in the market to buy a home, I help DFW residents alleviate the stress of buying for the best possible price in the least amount of time.

Real Estate Reflections •

September 21, 2022

Will My House Still Sell in Today’s Market?

If recent headlines about the housing market cooling and buyer demand moderating have you worried you’ve missed your chance to sell, here’s what you need to know. Buyer demand hasn’t disappeared, it’s just eased from the peak intensity we saw over the past two years.

Buyer Demand Then and Now

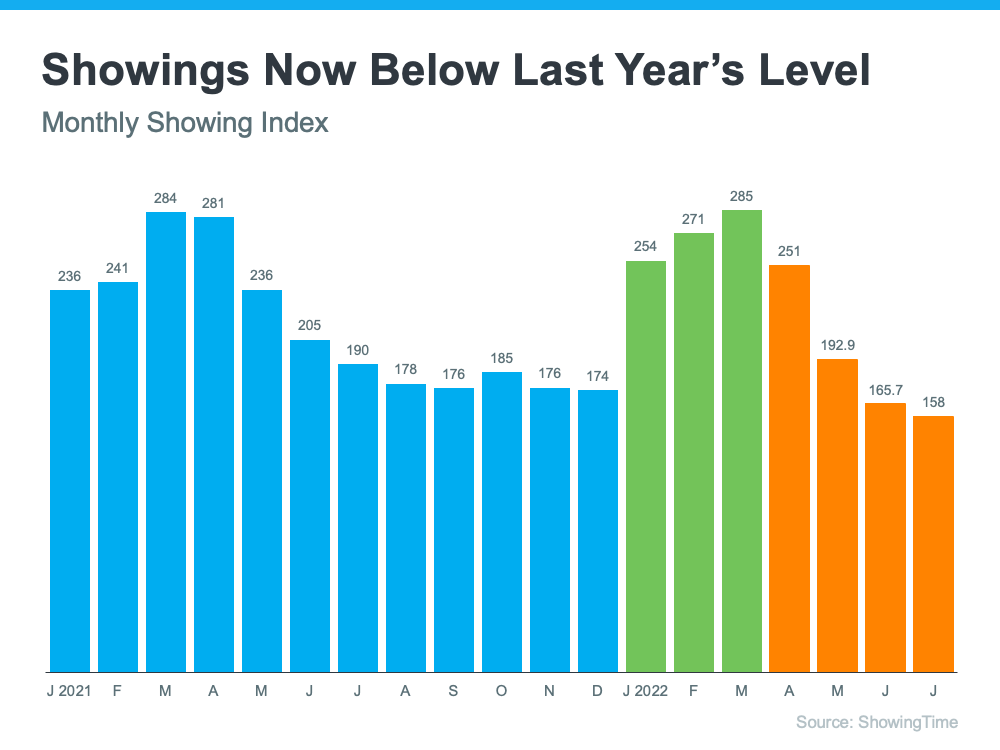

During the pandemic, mortgage rates hit record lows, and that spurred a significant rise in buyer demand. This year, as rates increased due to factors like rising inflation, buyer demand pulled back or softened as a result. The latest data from ShowingTime confirms this trend (see graph below):

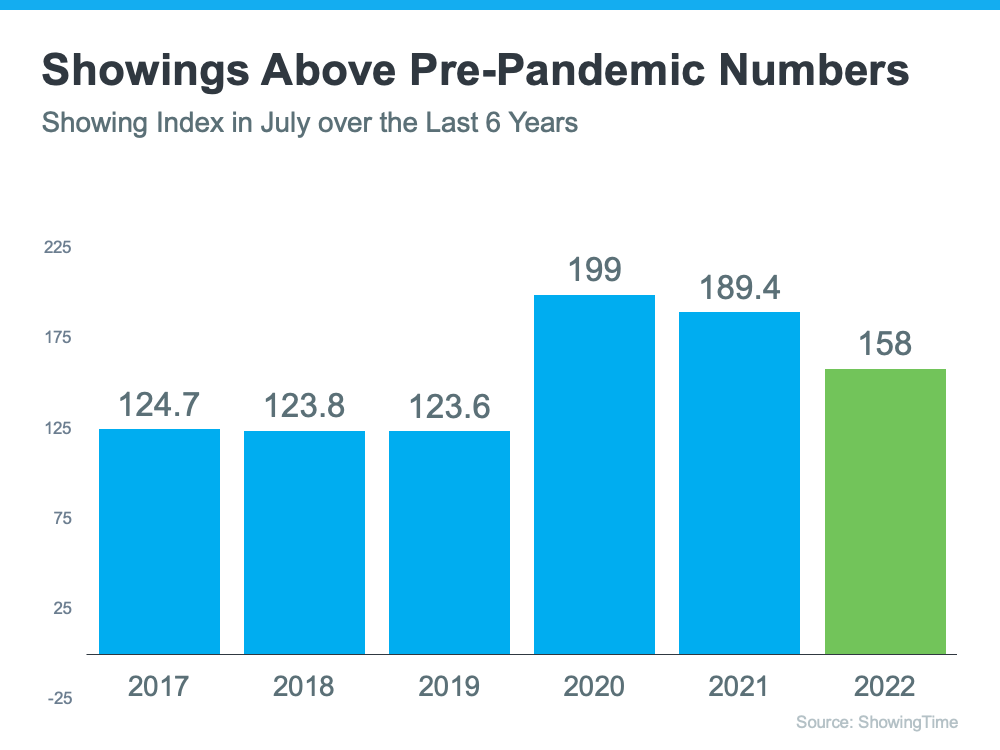

The orange bars in the graph above represent the last few months of data and the clear cooldown in the volume of home showings the market has seen since mortgage rates started to rise. But context is important. To get the full picture of where today’s demand stands, let’s look at the July data for the past six years (see graph below):

This second visual makes it clear that, while moderating compared to the frenzy in 2020 and 2021, showing activity is still beating pre-pandemic levels – and those pre-pandemic years were great years for the housing market. That goes to show there’s still demand if you sell your house today.

What That Means for You When You Sell

The key to selling in a changing market is understanding where the housing market is now. It’s not the same market we had last year or even earlier this year, but that doesn’t mean the opportunity to sell has passed.

While things have cooled a tad, it’s still a sellers’ market. If you work with me your trusted local expert to price your house at the current market value, the demand is still there, and it should sell quickly. According to a recent survey from realtor.com, 92% of homeowners who sold in August reported being satisfied with the outcome of their sale.

Bottom Line

Buyer demand hasn’t disappeared, it’s just moderated this year. If you’re ready to sell your house today, let’s connect so you have expert insights on how the market has shifted and how to plan accordingly for your sale.

Real Estate Reflections •

September 12, 2022

Expert Forecasts on Mortgage Rates

If you’ve been thinking of buying a home, you may have been watching what’s happened with mortgage rates over the past year. It’s true they’ve risen dramatically, but where will they go from here, especially as the market continues to slow?

As you think about your homeownership goals and decide if now’s the time to make your move, the best place to turn to for that information is the professionals. Here’s a summary of the latest mortgage rate forecasts from housing market experts.

Experts Project Mortgage Rates Will Stabilize

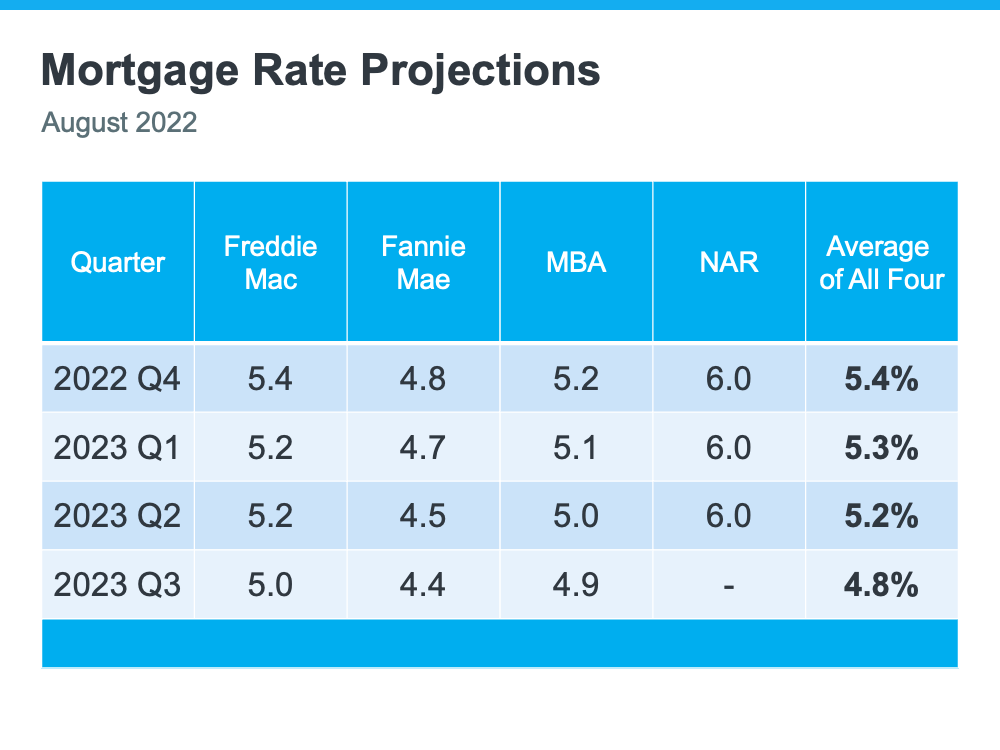

While mortgage rates continue to fluctuate due to ongoing inflationary pressures and economic uncertainty, experts project they’ll start to stabilize in the months ahead. According to the latest projections, mortgage rates are expected to hover in the low to mid 5% range initially, and then potentially dip into the high 4% range by later next year (see chart below):

That could bring you some welcome relief. So far this year, mortgage rates have climbed over two percentage points due to the Federal Reserve’s response to inflation, and that’s made it more expensive to buy a home. And wondering if the rise in rates will continue is keeping some prospective buyers on the sidelines.

But now that experts say mortgage rates should stabilize, this gives you a bit more certainty about what they think the future holds, and that may help you feel more confident about your decision to buy a home.

Bottom Line

Whether you’re looking to buy your first home, move up to a larger home, or even downsize, you need to know what’s happening in the housing market so you can make the most informed decision possible. Let’s connect to discuss your goals and determine the best plan for your move.